Tesla's Q3 Earnings: Decoding the Price Drop and Tesla's Real Future

The Financial Quarter Everyone Is Misunderstanding

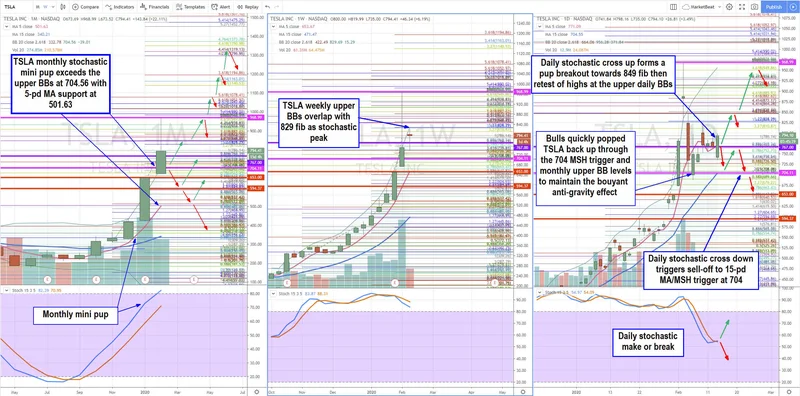

Let’s be honest. When TSLA Earnings: Tesla Reports 31% Drop in Q3 Earnings amid Record Revenue dropped, you could almost hear the collective gasp from Wall Street. The stock ticker flickered in after-hours trading like a nervous heartbeat. The headlines screamed about a 31% drop in profits and a miss on earnings-per-share estimates. Analysts furrowed their brows over contracting operating margins, down to 5.8% from 10.8% a year ago. On the surface, it looked like a classic case of a high-flying company hitting some serious turbulence.

But looking at this report and seeing only trouble is like staring at a blueprint for a spaceship and complaining about the cost of titanium. It completely misses the point. What I saw in those numbers wasn't a story of decline; it was the financial echo of a company in the middle of one of the most audacious pivots in modern industrial history.

The critics are fixated on the cost. They see the dip in margins and attribute it to tariffs, sales mix, and the usual suspects of manufacturing. And sure, those factors are there. But the real story, the one hiding in plain sight in Tesla's own report, is the "increased investment in AI and R&D." This isn't a sign of weakness; it's the cost of building the future. When I saw that free cash flow number, I honestly had to read it twice. A record $3.99 billion. That’s not the balance sheet of a car company struggling with costs; it's the war chest of a technology giant funding its next act.

So, while the rest of the world is busy dissecting the past, let's talk about what Tesla is actually building with all that cash. What does this quarter really signal for the decade ahead?

The End of the Car Company

For years, we’ve been conditioned to see Tesla as a car company—a very successful, very disruptive car company, but a car company nonetheless. We measure it by deliveries, by vehicle margins, by how many Model Ys it can push out of its factories. This Q3 report is, in my opinion, the clearest signal yet that this framework is becoming obsolete.

Tesla is using its incredibly profitable hardware business as an engine to fuel a metamorphosis into something else entirely: a full-stack AI and robotics company. Think of the car division as the launchpad. It generates the capital, the data, and the engineering expertise needed for the real mission. The company stated it plainly: "we expect our hardware related profits to be accompanied by an acceleration of AI, software and fleet-based profits." That’s not a throwaway line in an earnings report; it’s a mission statement. It’s the sound of the chrysalis cracking.

This is the kind of breakthrough that reminds me why I got into this field in the first place—the sheer audacity of it is just staggering. You can see the pieces moving into place: they’re installing the first production lines for the Optimus humanoid robot while simultaneously confirming that the Cybercab and Tesla Semi are on track for 2026. This isn't just about diversifying revenue streams. This is about building an entirely new industrial and logistical ecosystem from the ground up—an ecosystem where autonomous robots build the autonomous vehicles that are run by the autonomous software, all learning from each other in a virtuous cycle.

This is a transition as profound as Amazon’s shift from an online bookstore to the backbone of the internet with AWS. In the early 2000s, people fixated on Amazon's thin retail margins, completely missing that Jeff Bezos was building a global computing infrastructure in the background. Does that sound familiar? The market is looking at Tesla’s automotive margins while Elon Musk is building the infrastructure for physical-world autonomy.

Of course, with this kind of power comes an almost terrifying level of responsibility. Deploying millions of autonomous vehicles and humanoid robots into the world isn't just an engineering challenge; it's a profound ethical one. How do we ensure these systems are safe, unbiased, and serve humanity’s best interests? That's the question that should keep us all up at night, and one that requires a public conversation, not just a corporate one.

The real product is no longer the car. The car is becoming the vessel. The real products are the neural net, the robot, and the autonomous fleet. That fleet is where the second, and potentially larger, S-curve of revenue comes from. The company talks about "fleet-based profits"—that’s business-speak for a revolutionary idea. In simpler terms, it means the car continues to make money for Tesla long after you've bought it by operating as part of a shared, autonomous mobility network. Your car becomes an asset that works for you, and for Tesla. Is there any other automaker on the planet even thinking in these terms?

They're Building the Machine That Builds the Future

So, let's step back from the noise. Forget the knee-jerk reactions and the panicked headlines. This earnings report wasn't about a 31% drop in profit. It was about a 100% investment in a new reality. The dip in margins isn't a failure; it’s a down payment. Tesla is consciously sacrificing short-term profitability for the long-term goal of solving real-world autonomy. They are using billions in cash flow not to pad the next quarter, but to build the machine that will build the future. And if you’re still valuing them as just a car company, you’re looking in the rearview mirror.